Author

InfoGuard

The completely revised FINMA Circular 2023/1 on management of operational risks and ensuring resilience in banks and the reworked FINMA Circular 2013/3 on auditing come into effect as of 1 January 2024. The new FINMA Circular 2023/1 replaces the previous edition, 2002/21 “Operational risk – Banks”. This article provides the most important information about the new features and the expectations for financial institutions (banks, investment firms, finance groups and conglomerates).

In March 2021, the Basel Committee on Banking Supervision (BCBS) published the new Principles for Operational Resilience (POR) and the revised Principles for the Sound Management of Operational Risk (PSMOR). These principles should give financial institutions the ability to bettercope with operational threats. The publication of the above principles triggered a complete overhaul of the FINMA Circular which comes into effect as at 1 January 2024.

Based on the changes in FINMA Circular 2023/1, the FINMA Circular 2013/3 “Auditing” was also amended as follows:

New

Next, we can gain an overview of the total of eight principles of the new circular. In general, the principles apply to all addressees of the circular. However, in individual cases these depend on the size, complexity, structure and risk profile of the bank. The principle of proportionality applies. The eight major principles are summarised as follows:

1. Comprehensive management of operational risks (Rz 22-46)

2. Comprehensive management of ICT risks (Rz 47-60)

Guaranteeing suitable processes, procedures, responsibilities and resources:

3. Management of cyber risks (Rz 61-70)

Guaranteeing suitable processes, procedures, responsibilities and resources:

4. Management of critical data risks (Rz 71-82)

5. Business Continuity Management (BCM) (Rz 83 – 96)

6. Management of risks from international service business (Rz 97-100)

7. Guaranteeing operational resilience (Rz 101-111)

8. Transition periods

The new FINMA Circular 2023/1 defines important requirements for financial institutions, some of which are new. The new requirements focus in particular on the management of risks relating to critical data (not only customer data), the management of ICT risks, the establishment of an appropriate Business Continuity Management system and guaranteeing operational resilience.

FINMA Circular 2023/1 - the management of operational risks - also specifies the responsibilities of the board of directors and the management. In terms of the requirements, it should be noted that there are relaxations for banks and investment firms in supervisory category 4 and 5 and for banks classed as small banks and investment firms which do not hold accounts.

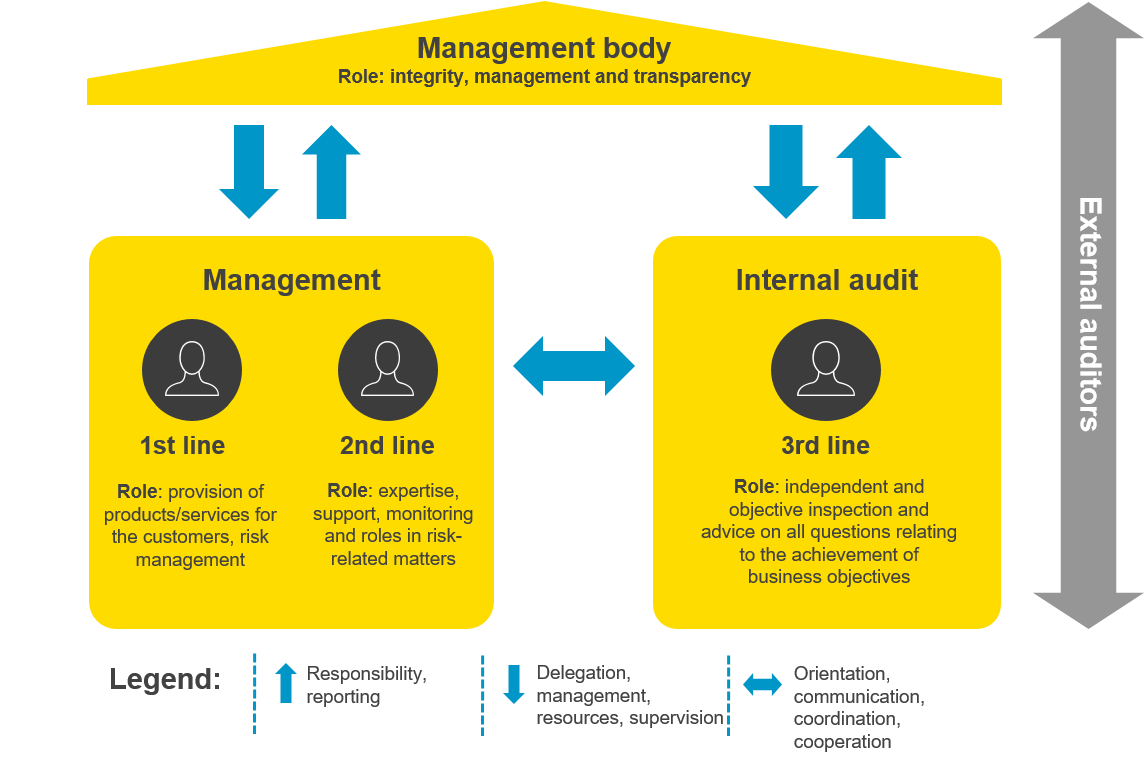

An important tool for efficient and effective management of (operational) risks involves dividing the roles, expertise and responsibilities (RER) into different lines of defence:

First line of defence

The first line of defence lies with the business and process officers. The operative management is responsible for the maintenance of effective internal controls and carrying out risk and check processes during everyday business. This includes identification and assessment of controls and reduction of risks. The business and process officers are also responsible for the development and implementation of internal guidelines and procedures. They make sure that the activities tally with the organisational objectives.

Second line of defence

The second line of defence supports the management in order to ensure that the risks and controls are being properly managed. The management sets up different risk management and compliance functions in order to support the structure and/or the monitoring of the controls in the first line of defence. The second line of defence fulfils an important purpose but cannot be completely independent because of its management function.

Third line of defence

The third line of defence gives the management and the board of directors the peace of mind that the efforts of the first two lines comply with the business objectives. The main difference between the third line of defence and the first two is the high degree of organisational independence and objectivity. Internal auditing cannot arrange or implement processes, but it can give advice and recommendations on processes. Internal auditing can also support the company’s risk management system, but it can only implement or execute risk management within its own function. Internal auditing achieves its objectives by means of a systematic approach to evaluating and improving the effectiveness of the risk management, control and governance processes.

External auditors

External auditors are responsible for submitting an assessment on the orderliness (correctness within a specific degree of significance) of the annual reports in compliance with specific accounting standards. External auditors can also provide guarantees on compliance with institutional regulations to the regulatory body.

The IIA Three Line Model (Source: The Institute of Internal Auditors)

For some financial institutions, there is a lot of catching-up to do in order to meet the transition periods. While the entry into force as at 1 January 2024 incorporates transition periods of up to two years, financial institutions are well advised to get to grips with the new requirements as soon as possible in order to guarantee appropriate compliance within the deadlines.

Financial institutions which have already implemented best practice standards in risk and business continuity management should be looking at a more manageable outlay. FINMA Circular 2023/1 specifies the responsibilities of the board of directors and the management and requires coordination and communication.

How are things looking for you?

In your company, are the responsibilities with respect to the handling of operational risks adequately clear and defined?

Have the threat scenarios for your company been identified and formulated?

Do you carry out regular analyses of operational risks?

Have you defined and implemented processes for change management, ICT operational management, incident management, etc.?

Do you carry out regular vulnerability analyses, penetration tests and cyber practices (e.g. table top exercise, red teaming exercises, etc.)?

Is there a BCM strategy identifying critical business processes in your company in line with Business Impact

Analyses (BIA), have you defined Recovery Time Objectives (RTO) and Recovery Point Objectives (RPO) and drawn up Business Continuity Plans (BCP) and Disaster Recovery Plans (DRP)?

Do you test the critical functions regularly in line with their interruption tolerances?

Do you provide your employees with regular training on their responsibilities in handling cyber risks?

etc.

Thanks to our many years of proven experience in security consultancy, we are happy to support you on ensuring compliance with the new FINMA Circular 2023/1.

1 Critical data is data which is of such significance given the size, complexity, structure, risk profile and business model of the institution that it requires increased security. This is data that is critical to the successful, lasting provision of the services by the institute or for regulatory purposes. Confidentiality, integrity and availability must all be considered when assessing and determining the criticality of data. Each of these three aspects can be key in determining whether data is classified as critical (Source: FINMA Circular 2023/1).